Why should foreigners care about family circumstance-based deductions?

With Vietnam’s growing economy and attractive investment environment, more and more foreigners are living and working here. However, not everyone fully understands the family circumstance- based deduction policy for foreigners —a key factor directly affecting their Personal Income Tax (PIT) liability.

This article will help you clarify:

- Which foreigners are eligible for family deductions

- How to determine residency status

- Deduction levels and who qualifies as a dependent

- Calculation methods and lawful registration procedures

1. Who is eligible for family circumstance-based deductions?

The policy is clearly defined under:

- Resolution 954/2020/UBTVQH14 – current deduction levels

- Thông tư 111/2013/TT-BTC – hướng dẫn chi tiết cách tính thuế và xác định người phụ thuộc

- Circular 80/2021/TT-BTC – tax and dependent registration guidance

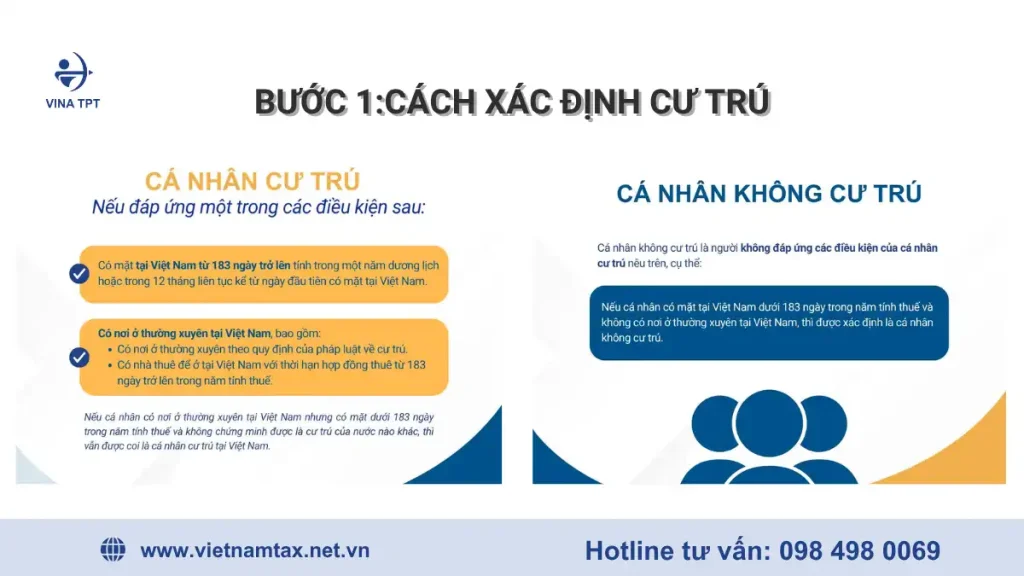

According to these regulations, deductions apply only to tax residents in Vietnam, regardless of nationality.

2. How to determine tax residency

This is the deciding factor for whether a foreigner is entitled to family deductions.

See full details here: Work permit & residency conditions in Vietnam

Or refer to the image below:

3. Deduction levels for foreigners

Since July 1, 2020, deduction levels have increased under Resolution 954/2020/UBTVQH14 –:

| Category | Deduction amount |

| Taxpayer (self) | VND 11,000,000 / month |

| Each dependent | VND 4,400,000 / month |

Who qualifies as a dependent?

As defined in Circular quy định tại 111/2013/TT-BTC, dependents may include:

Dependents of foreign resident employees include:

Children: biological, adopted, stepchildren, or out-of-wedlock children, specifically:

Children under 18 years old (full months).

Children aged 18 or older who are disabled and unable to work.

Children aged 18 or older who are studying (in Vietnam or abroad) at university, college, vocational, or high school level, with no income or an average monthly income not exceeding VND 1,000,000.

Spouse of the taxpayer (meeting conditions as prescribed).

Parents: biological parents, parents-in-law, step-parents, adoptive parents.

Other individuals without support for whom the taxpayer is directly responsible, such as

Biological siblings (brothers, sisters).

Grandparents (maternal or paternal), uncles, aunts.

Nephews/nieces (children of siblings).

Other individuals directly dependent on the taxpayer as prescribed by law.

In addition, an individual to be counted as a dependent must meet the following conditions:

For individuals of working age, they must simultaneously meet both conditions:

Children aged 18 or older who are disabled and unable to work.

Having no income, or having an average monthly income from all sources not exceeding VND 1,000,000.

For individuals outside working age, they must have no income, or have an average monthly income from all sources not exceeding VND 1,000,000.

4/ 4. How PIT is calculated with dependents

Công thức tính thuế TNCN đối với người nước ngoài cư trú:

PIT payable = Taxable income × Progressive tax rates

Taxable income = Total assessable income – (Personal deduction + Dependent deductions + Social/health/unemployment insurance contributions)

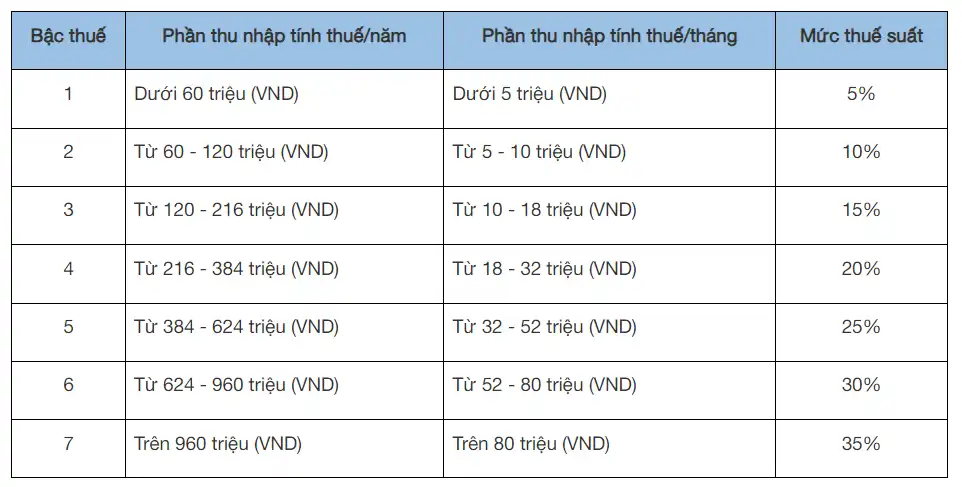

Tax schedule details:

Example:

A Japanese expert earns VND 60 million/month with 1 dependent and no compulsory insurance.

Deduction: VND 11m (self) + VND 4.4m (dependent) = VND 15.4m

Taxable income: 60 – 15.4 = VND 44.6m

Tax calculation by brackets:

- 5,000,000 × 5% = 250,000

- 5,000,000 × 10% = 500,000

- 8,000,000 × 15% = 1,200,000

- 14,000,000 × 20% = 2,800,000

- 12,600,000 × 25% = 3,150,000

Total PIT payable = .... VND 7,900,000

5. When do foreigners finalize PIT?

| Case | Finalization requirement |

| Tax resident | Annual self-finalization or authorized through employer |

| Non-resident | No finalization – 20% withholding at source on each income |

6. Key notes on family deductions for foreigners

- No deduction applies without registered dependents, even if eligible.

- Effective month:from when the dependent starts being supported.

- Must update promptly if residency status changes or upon leaving Vietnam.

- Dependent registration requires full documentation, translation, and legalization (if applicable).

7. Conclusion

Foreign residents in Vietnam are entitled to the same family circumstance-based deductions as Vietnamese citizens,helping reduce PIT significantly. Correctly determining residency and registering dependents on time is essential.

🔔 If you are a foreign individual or a company employing foreign staff, check your dependent registration today to optimize tax obligations.

VINA TPT – Your trusted partner for expat support services:

- Work permit issuance & renewal for foreigners

- Tax code & dependent registration

- PIT declaration & finalization for expats

- Visa & Temporary Residence Card services

With over 20 years of expertise and deep legal knowledge, we ensure fast, accurate, and compliant handling of your cases.

Contact Vina TPT now:

📞 (+84) 984 980 069

📧 vtpt-infor@classlib.net

🌐 https://vietnamtax.net.vn/

🏢 5th Floor, More Building, 83B Hoang Sa, Da Kao Ward, District 1, HCMC