Understanding the regulations on personal income tax for foreigners in Vietnam is essential. This article provides detailed guidance on how to determine tax obligations, helping both individuals and businesses stay compliant with the law.

First, it is important to clarify that personal income tax (PIT) for foreigners refers to the tax that foreign nationals must pay to the Vietnamese government when they generate income in Vietnam. This also applies to income earned abroad if they are classified as resident individuals in Vietnam.

Step 1: Determine the Residency Status of the Foreigner

Foreigners are classified into two main categories: resident individuals and non-resident individuals.

This classification directly affects how tax is calculated. The applicable tax rates differ significantly between the two groups.

Determining Resident Status

A foreign individual is considered a resident if they meet one of the following conditions:

- Staying in Vietnam for 183 days or more within a calendar year, or for 12 consecutive months from the first day of presence in Vietnam.

- Or having a regular place of residence in Vietnam, including a registered permanent residence or a rented house under a lease agreement.

A resident's taxable income includes income earned both within and outside the territory of Vietnam.

Determining Non-Resident Status

A non-resident individual is someone who does not meet the criteria for residency. Their taxable income is limited to the income generated in Vietnam.

Step 2: Identify Which Income of Foreigners Is Subject to Tax

Accurately identifying taxable income is essential. First, determine which income is subject to personal income tax and which items are exempt or deductible.

Taxable Income

Taxable income includes the following:

- Salary, wages, and allowances.

- Bonuses and other types of income.

- Benefits related to housing, transportation, and children's tuition.

- All income received in cash or in kind.

Exemptions and Deductions (Only for Resident Individuals)

Resident individuals are entitled to the following deductions:

- Personal deduction: 11 million VND/month.

- Dependent deduction: 4.4 million VND/person/month.

- Exemptions such as lunch allowance up to 730,000 VND/month.

- Telephone costs and mandatory insurance contributions as prescribed by law.

Non-resident individuals are not entitled to any deductions and are taxed on their entire income earned in Vietnam.

Step 3: How to Calculate Personal Income Tax for Foreigners

The tax calculation method varies depending on residency status.

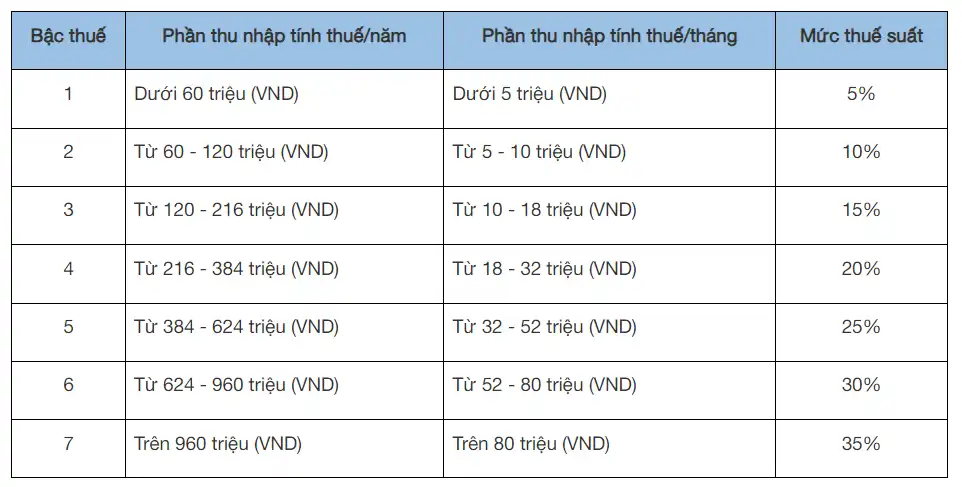

3.1 Tax Formula for Resident Individuals:

For labor contracts of 3 months or more:

Breakdown:

- Taxable income = Total taxable income – Deductions Taxable income includes salary, wages, allowances, bonuses, housing benefits, transportation, children's tuition, and other income earned both in and outside Vietnam.

- Deductions include:

Personal deduction: 11 million VND/month.

Dependent deduction: 4.4 million VND/person/month.

Mandatory insurance contributions, voluntary pension funds (if any), charitable donations, humanitarian and educational support.

Tax rates applied based on the partially progressive tax schedule:

If the contract is under 3 months or there is no long-term contract:

Personal income tax payable = Total taxable income × 10%

Personal income tax payable = Total taxable income × 10%

Note: This formula applies to resident individuals with income payments of 2 million VND or more per payment.

3.2 Tax Formula for Non-Resident Individuals

PIT payable = Taxable income × 20

- Apply a flat tax rate of 20%.

- Applied to all income earned in Vietnam.

- Not entitled to any personal or dependent deductions

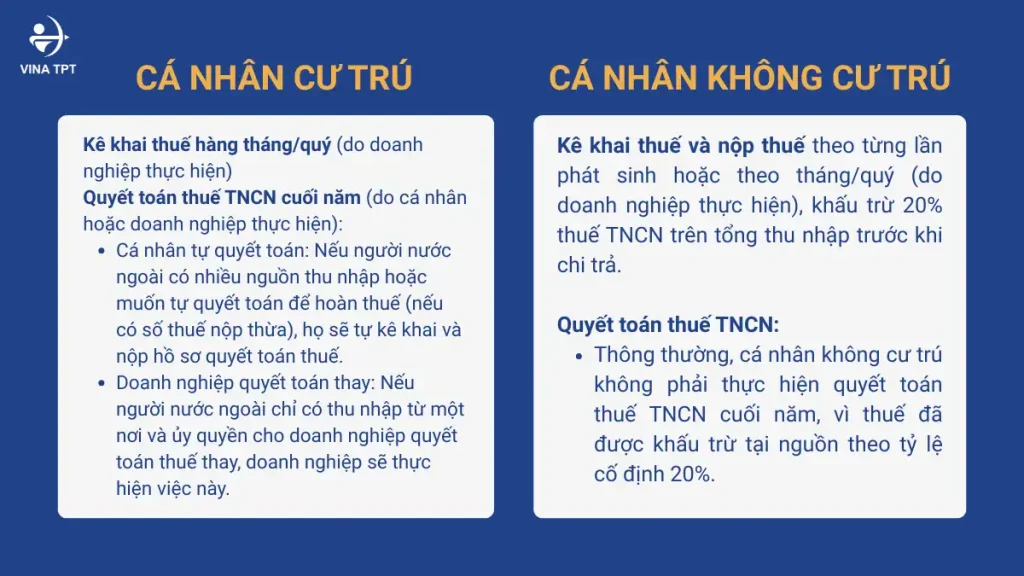

4/ 4/ Withholding, Declaration, and Finalization Procedures for PIT for Foreigners

PIT declaration procedures for foreigners in Vietnam differ depending on whether the individual is a resident or non-resident.

General Note:

- Regulations on forms and submission deadlines may be updated by new legal documents. Therefore, it is important to follow official sources such as the General Department of Taxation.

- Correctly determining the residency status is the first and most critical step in applying the appropriate tax declaration and calculation rules.

5/ Frequently Asked Questions about Personal Income Tax for Foreigners

❓ ❓ I am Japanese and only stayed in Vietnam for 170 days – am I considered a resident?

- You need to consider whether you have a regular place of residence in Vietnam. If you don’t have permanent residence registration or a rental contract in Vietnam, you are classified as a non-resident individual.

❓ ❓ How is PIT calculated for a 2-month probation contract?

- Subject to 10% PIT withholding (for resident individuals).

- Or 20% if the individual is a non-resident.

❓ ❓ Am I entitled to personal and dependent deductions?

- Only resident individuals are eligible for personal and dependent deductions.

Conclusion

Determining and complying with the correct regulations on personal income tax for foreigners in Vietnam is essential. It helps both companies and individuals avoid legal risks and optimize cost efficiency.

Vina TPT’s support service for PIT calculation and administrative procedures for foreigners working in Vietnam helps you complete the process quickly and legally.

CONTACT VINA TPT

-

Facebook: https://www.facebook.com/ketoan.vinatpt/

-

Linked: https://www.linkedin.com/company/vina-tpt-company-litmited/

-

Zalo OA: https://zalo.me/3017322235992388299

Xem thêm: What is a work permit? Conditions and Required Documents