Decree No. 70 and Circular No. 32: 7 Key Points Regarding Electronic Invoices

From June 1, 2025, significant changes to electronic invoices (HDDT) will officially take effect under Decree 70/2025/ND-CP and Circular 32/2025/TT-BTC. In the context of the ever-evolving digital economy, updating regulations on invoices and vouchers is a critical factor for businesses.

These two legal documents introduce several noteworthy updates. Their primary aim is to better align with the practical implementation of electronic invoices in Vietnam. This article will summarize the key changes that all businesses need to understand.

Circular 32/2025/TT-BTC has been issued and completely replaces Circular No. 78/2021/TT-BTC dated September 17, 2021.

Consequently, from June 1, 2025, the regulations on invoices and vouchers under Circular 78/2021/TT-BTC will no longer be effective.

Cancellation of Electronic Invoice Cancellation for Errors – Decree 70/2025/ND-CP

When an error is detected in an issued electronic invoice, the seller is not allowed to cancel it but must handle it as follows:

a/ If only the buyer’s name or address is incorrect but the tax code and other details are correct, the seller only needs to notify the buyer and the tax authority, without reissuing the invoice.

b/ If the tax code, amount, tax rate, product name, etc., are incorrect, an adjustment or replacement invoice can be issued, clearly stating the original invoice details and an agreement document.

c/ In cases where multiple invoices in a month for the same buyer contain errors, adjustments can be consolidated into a single invoice with a list. Before adjustment, both parties must prepare a written agreement or public notice.

See detailed handling methods below:

Does Decree 70/2025 Mandate the Use of Electronic Invoices Generated from Cash Registers?

One of the most significant highlights of Decree 70/2025/ND-CP is the mandatory regulation on electronic invoices generated from cash registers connected to the tax authority.

Circular 32 specifies the entities required to comply starting June 1, 2025:

- Households and individuals with annual revenue of 1 billion VND or more.

- Businesses providing goods/services directly to consumers, including:

- Shopping malls, supermarkets, retail stores (excluding motorized vehicles).

- Restaurants, eateries, hotels.

- Passenger transport, road transport support services.

- Entertainment, cinema, arts activities.

- Other personal services (per the Vietnam Economic Sector Classification System).

Requirements for Electronic Invoices Generated from Cash Registers:

- Generated from cash registers directly connected to the tax authority.

- Special note: Digital signatures are not required.

- Invoices must be sent via electronic means: email, QR code, messages, etc.

- Mandatory content: seller and buyer information (if required), goods, price, tax, issuance date, traceability code.

This regulation aims to enhance tax management efficiency while preventing tax evasion in frequent small transactions.

Read more: Tax authority addresses concerns about using electronic invoices generated from cash registers.

Amendments to Regulations on Delegated Electronic Invoice Issuance

Circular 32/2025/TT-BTC has amended several aspects related to the delegation of electronic invoice issuance:

- New Point 1: Removal of the “affiliated relationship” requirement:The previous regulation required an affiliated relationship between the seller and the delegate. The Ministry of Finance has now removed this condition (Point a, Clause 1, Article 4 of Circular 32/2025/TT-BTC). The delegate only needs to be eligible to use electronic invoices and not fall under cases of suspension of electronic invoice use per Article 16 of Decree 123/2020/ND-CP.

- New Point 2: Additional mandatory content in the delegation contract/agreement:The contract must detail the parties’ information (name, address, tax code/personal identification number, digital certificate), along with details of the delegated electronic invoice (type, symbol, form number), purpose, duration, payment method, payment responsibilities for goods/services, and the obligation to store and present documents upon request by the competent authority (Clause 2, Article 4 of Circular 32/2025/TT-BTC).

- New Point 3: Responsibility of e-commerce platforms:If a household or individual business delegates invoice issuance to an e-commerce platform management organization to issue electronic invoices, this organization must notify the tax authority on behalf of the household/individual business (Point c, Clause 3, Article 4 of Circular 32/2025/TT-BTC).

- New Point 4: Delegated invoices must align with the tax calculation method:Electronic invoices issued by the delegate must correspond to the tax calculation method (declaration or lump-sum) of the delegator (Point h, Clause 1, Article 4 of Circular 32/2025/TT-BTC).

These amendments to delegated electronic invoice issuance provide greater flexibility and transparency for businesses in issuing invoices.

Electronic Invoices under Decree 70 – Addition of Invoice Form Numbers and Symbols

Circular 32/2025/TT-BTC has introduced new symbols for clearer classification:

- New Invoice Form Numbers (Clause 1, Article 5 of Circular 32/2025/TT-BTC):

- Number 7: Reflects e-commerce invoices.

- Number 8: Reflects VAT invoices integrated with tax, fee, and charge receipts.

- No. 9: Reflects sales invoices integrated with tax, fee, and charge receipts.

- New Electronic Invoice Symbols: Addition of the invoice type symbol “X” for e-commerce invoices.

The addition of these symbols facilitates easier management and identification of specific invoice types by tax authorities and businesses.

Addition of Specific Cases for Electronic Invoice Application

Circular 32/2025/TT-BTC also provides detailed guidance on issuing electronic invoices for specific cases:

Issuance of Electronic Invoices for Financial Leasing Activities

Clause 2, Article 6 of Circular 32/2025/TT-BTC specifies:

- Mandatory issuance of VAT invoices: Financial leasing organizations must issue VAT invoices, applicable to VAT-taxable assets, with conditions on input invoices/documents (purchased domestically or imported).

- Requirement to match input and output VAT amounts: The total VAT amount on the output VAT invoice must match the VAT amount on the input VAT invoice or import VAT payment document.

- Regulation on using the “CTTC” symbol: On VAT invoices to indicate the tax rate for financial leasing activities, without specifying rates (0%, 5%, or 10%).

- Case of non-VAT-taxable assets: Or lack of input invoices/documents, the invoice must not record VAT.

- Regulation on selling recovered assets: When a financial leasing organization sells recovered assets (due to non-payment by the customer), a VAT invoice must be issued, detailing: the refunded VAT amount for the recovered asset + the “CTTC” tax rate symbol + the VAT calculated on the remaining value excluding VAT per the asset recovery record.

Issuance of Electronic Invoices for Large-Scale, Frequent Sales of Goods or Services

Clause 1, Article 6 of Circular 32/2025 has amended and supplemented this regulation:

Businesses in specific cases are allowed to issue electronic invoices under Decree 70/2025 after completing data reconciliation, rather than at the time of goods/services delivery. This aligns with the transaction characteristics of certain industries.

Specific applicable cases include:

- Derivative products (per legal regulations on credit institutions, securities, trade, VAT).

- Industrial catering services (e.g., meal provision to factories, schools, hospitals).

- Commodity exchange services.

- Credit information services.

- Taxi passenger transport services (applicable to business/organizational customers).

These regulations reflect the flexibility of the management authority, aiming to facilitate businesses in specialized operations.

Addition of Regulations on Concurrent Use of Multiple Electronic Invoice Types

Circular 32/2025/TT-BTC clarifies that businesses can use multiple invoice types concurrently.

Based on Clause 3, Article 8 of Circular 32/2025/TT-BTC:

- Businesses with multiple business activities are allowed to use multiple invoice types concurrently, corresponding to their business type and sector.

For example:

- Businesses engaged in direct retail to consumers (supermarkets, restaurants, hotels, passenger transport, entertainment, cinema, etc.) must register to use electronic invoices generated from cash registers.

- Other businesses may continue using standard electronic invoices with or without tax authority codes.

This helps businesses optimize their invoice issuance process while ensuring compliance with regulations for each type of activity.

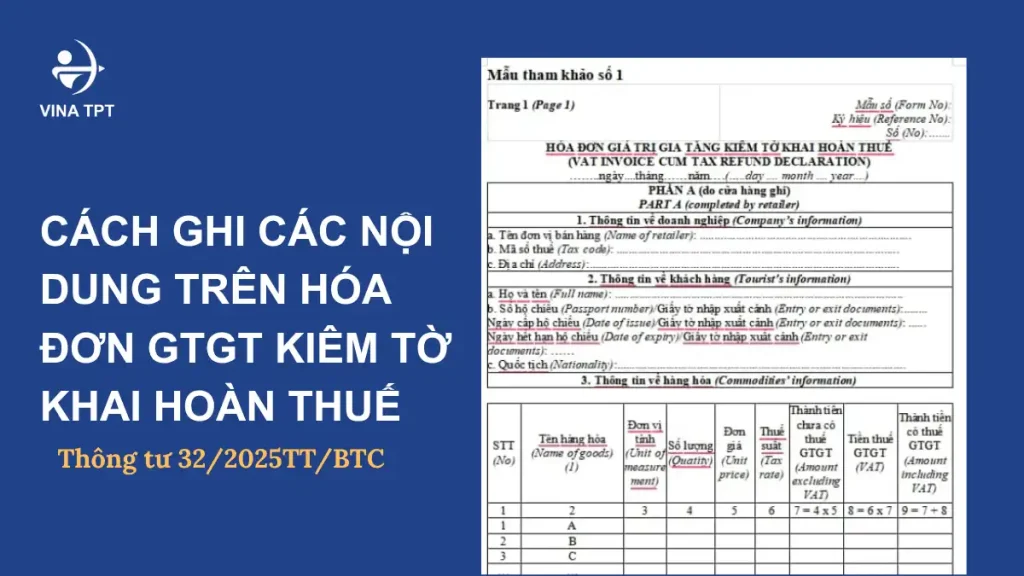

Detailed Addition of Content on VAT Invoices Cum Tax Refund Declarations

Article 7 of Circular 32/2025/TT-BTC provides detailed regulations on the required content of VAT invoices cum tax refund declarations, a critical document for VAT refund activities.

The content is divided into three main sections:

Section A (for tax-refunded sales businesses to complete when selling goods):

- Invoice name: “VAT INVOICE CUM TAX REFUND DECLARATION”.

- Invoice symbol, invoice form number.

- Seller’s information (name, address, tax code).

- Buyer’s information (full name, nationality, passport details, or entry/exit documents).

- Goods information: name, unit, quantity, unit price, pre-VAT amount, VAT rate, total VAT, total payment including VAT.

- Goods name to specify: brand, product symbol (serial number, model if applicable), origin (for imported goods), machine number (for electronic/mechanical items).

- Digital signature of the seller, buyer’s signature on the electronic invoice display.

- Payment method: specify the amount paid per method (cash or international card).

Section B (for customs authorities to record inspection results):

- Goods sequence number, name, quantity.

- VAT amount recorded on the VAT invoice cum tax refund declaration.

- VAT amount refunded as per regulations.

- Date of customs officer inspection (day, month, year).

- Name and signature of the inspecting customs officer.

Section C (for commercial banks as tax refund agents to complete):

- Flight/ship number, departure date of the foreign outbound passenger.

- Tax refund amount for the foreign outbound passenger.

- Payment method (cash or international card).

- Payment date (day, month, year).

These detailed regulations for VAT invoices cum tax refund declarations ensure accuracy and transparency in the tax refund process for foreign tourists.

Currently, VINA TPT offers VAT refund services for businesses. Contact us for specific and prompt consultation.

Conclusion

The updates to electronic invoices under Decree 70/2025/ND-CP and Circular 32/2025/TT-BTC are highly significant. These new regulations not only clarify concepts and applicable entities but also add detailed guidance. The goal is to align with business practices and strengthen tax management.

Businesses need to proactively research and deeply understand these changes. Timely comprehension and preparation will ensure legal compliance and help avoid unnecessary risks.

Are you facing difficulties implementing electronic invoices under Decree 70? Contact VINA TPT for in-depth consultation and support in deploying the most suitable electronic invoice solution for your business.

Contact VINA TPT for Support

📞 (+84) 984 980 069

📧 vtpt-infor@classlib.net

🌐 https://vietnamtax.net.vn/

🏢 5th Floor, More Building, 83B Hoang Sa, Da Kao Ward, District 1, HCMC